Messy Virgo decision pipeline, part 1: the AI investment council

AI fund management should not mean one model looks at a few charts and quietly decides what to buy.

That is too shallow for serious money management.

A real fund does not make isolated calls in a vacuum. It already holds positions. It carries risk. It operates under policy constraints. Every day it must decide what the portfolio should become, not just which tokens look interesting. When the decision involves real capital, the process itself must be legible, challengeable, and reversible.

Messy Virgo is building an AI investment council: a governed, board-style workflow where the fund receives preparation material, different portfolio-manager agents bring distinct investment views, risk is reviewed explicitly, decisions are recorded through motions and votes, and only certified outcomes can move into planning and execution.

In that model, Messy Virgo is not just a chatbot sitting next to the product.

Messy Virgo is the fund manager’s assistant and the visible identity of the process: the avatar that helps convene the meeting, surface the preparation material, collect human input, and later summarize what the council decided.

The council itself is not a free-form group chat. It is a structured workflow.

This post is part 1 of a short series. It explains the high-level idea: how Messy Virgo moves from market evidence to an AI-led investment council, and from there toward controlled portfolio action.

Note: This reflects where we are headed, not a frozen manual. The system is moving quickly, and implementation details may change. The important idea is the governance model: evidence, preparation, council debate, resolution, planning, and execution should remain separate.

The limits of a single answer

A single AI recommendation is tempting because it feels simple.

But simplicity can hide the wrong things.

In real portfolio management, different investment styles legitimately disagree for good reasons:

- a value-oriented manager may like a token whose price momentum is weak

- a momentum manager may want to ride a trend that looks expensive on fundamentals

- a macro-tactical manager may want lower beta exposure even while individual names look attractive

- a risk manager may accept the direction but challenge size, liquidity, or concentration

- the chair may agree with the thesis but reject the proposed implementation

Those disagreements are useful. They surface trade-offs that would otherwise stay hidden.

The mistake is to compress them into one opaque answer.

When capital is at stake, the decision needs to be inspectable. The rationale needs to be recorded. Dissent needs to be visible. A single model output or an unstructured agent conversation cannot deliver that by default.

That is why Messy starts with a small but structured council:

- Value & Quality PM — voting

- Macro-Tactical PM — voting

- Trend & Momentum PM — voting

- Risk Manager — non-voting

- Chair / Portfolio Constructor — non-voting

Over time, those roles can evolve into richer agents with their own methods, memory, and track records. Different funds may eventually invite different portfolio managers to the table. The point is not to eliminate disagreement. The point is to make it part of the process.

A governed council, not a chat room

The easiest way to understand the council is to imagine a company board meeting.

Before the meeting, executives do not receive a raw data dump and improvise from scratch. They receive a preparation pack: summaries, risks, policy boundaries, open questions, and the decisions that need to be made.

Then the meeting follows an agenda.

People have roles.

Some participants make recommendations. Some challenge risk. Some synthesize. Some vote. Some record the outcome.

Messy’s decision pipeline follows the same pattern.

At a high level, a council session moves through ten steps:

- Confirm the session can proceed.

- Review the preparation material.

- Discuss the broad fund posture.

- Review the current portfolio.

- Review candidates and possible rotations.

- Let each PM role state its view.

- Let Risk challenge the proposal.

- Let the Chair synthesize a motion.

- Vote.

- Record the Council Resolution.

The outcome is not a trade ticket. It is a certified resolution that captures what the council decided, including any recorded dissent.

A no-action outcome is valid. If the current portfolio still makes sense, the council should say so. Creating trades just because a meeting happened would weaken the process.

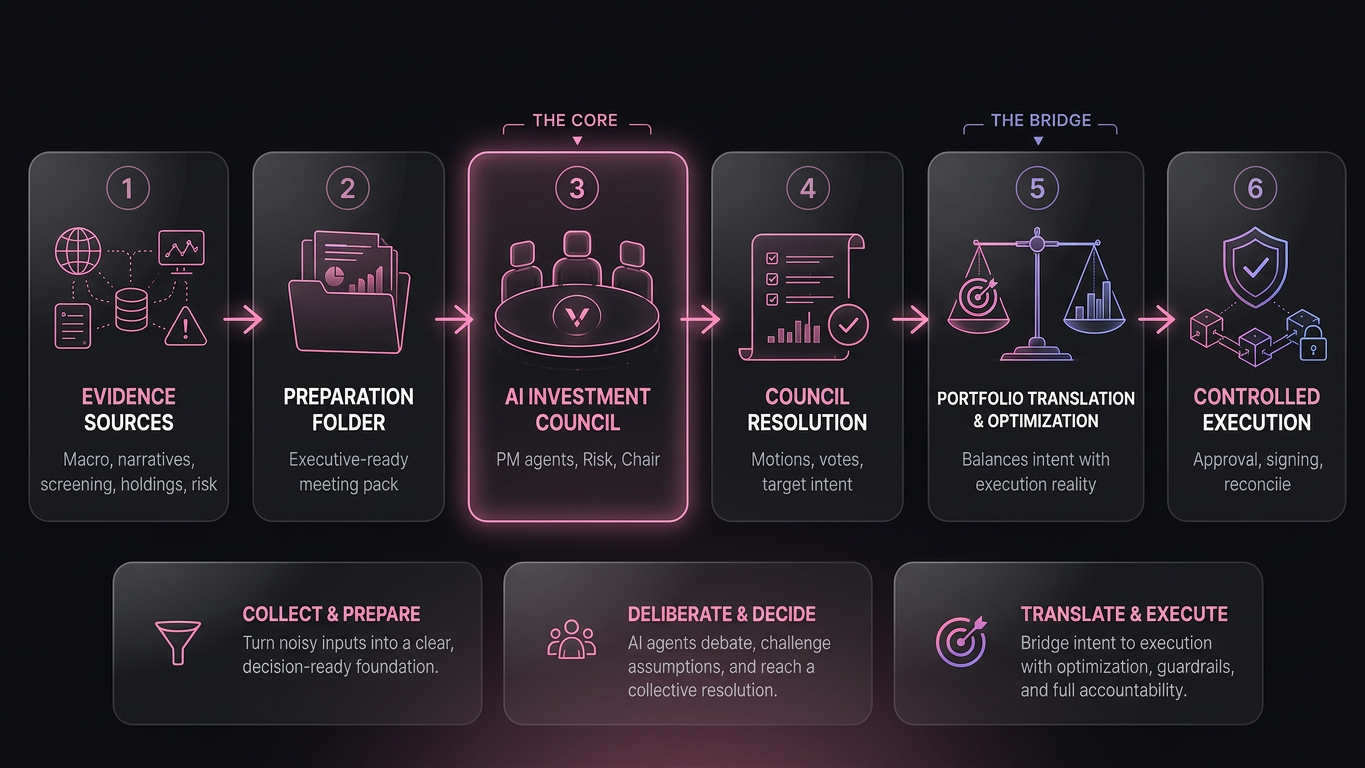

The six-stage decision pipeline

The council sits inside a larger pipeline. Each stage has a distinct purpose.

Evidence is assembled from multiple sources: macro context, narrative momentum, performance and technical signals, social attention, security and contract-risk data, current holdings, liquidity warnings, and prior decisions. Screening is one input among many.

Preparation turns that evidence into decision-ready material. The goal is not to dump more data. The goal is to surface what the council actually needs to decide.

Council is where the structured debate happens. PM agents state their views. Risk enforces policy. The Chair turns disagreement into a motion. The council votes and records a resolution.

Resolution is the official portfolio intent created by the meeting. It is not yet an execution plan.

Planning translates that intent into executable reality. It balances the council’s direction against costs, liquidity, reserves, and other constraints. The market is not frictionless; a directionally correct change can still be too small or too expensive to execute.

Controlled execution only proceeds through reviewable gates. Nothing moves into signing, submission, or reconciliation without passing the prior stages.

Each handoff exists for a reason. Remove any one, and the system either loses governance or loses practicality.

What this makes possible

The council model is not internal plumbing.

It is part of how Messy can eventually prove what it is building.

If the process works, public fund pages should be able to show more than NAV and holdings. They should show the governance trail: what evidence was reviewed, what the council discussed, what decision was made, whether there was dissent, which warnings were recorded, and how the decision moved through planning and safety gates.

That does not mean publishing every internal detail. It means producing public-safe summaries from a real process, instead of trying to generate a marketing narrative after the fact.

The same structure also changes what becomes possible for agent identities. A portfolio-manager seat can become a real agent slot with a name, an investment philosophy, scoped tools, fund-specific memory, a learning loop, and a history of prior decisions and outcomes. Over time, agents can be evaluated against the same rules. Their recommendations can be compared against results. Their strengths and weaknesses can become visible.

That is how the council becomes more than automation.

It becomes an investable governance surface.

What comes next (part 2)

Part 1 introduced the AI investment council: the board-style process where Messy Virgo helps convene preparation, PM agents deliberate, Risk checks policy, the Chair synthesizes, and the council records a resolution.

Part 2 will focus on the next layer: the decision-to-execution bridge.

A Council Resolution is not a trade ticket. We will explain how Messy thinks about translating portfolio intent into practical rebalance plans, why costs and constraints matter, and how solver-backed planning can help balance fund decisions against execution reality without turning execution into a black box.